Three days ago, the SEC made it clear that CFOs and management teams should be taking action to not only manage, but also to price climate risk. Similar to traditional financial reporting, climate-related risk reporting is complex and cannot be mastered overnight. The best approach? Start now. And make a climate risk assessment your first step in evaluating how climate risks and opportunities may affect current and future financial positions.

For a full summary of the proposed rule, please review our bulletin.

Get your roadmap in place

The full 510-page proposed rule is loaded with information, but companies have to start somewhere. So, we’ve boiled down the most important and pragmatic next steps for CFOs and their teams to help finance leaders begin taking action right away.

1. Conduct a Climate Risk Assessment

The first step to climate risk management is a climate risk assessment. A climate risk assessment is a systematic evaluation of potential hazards stemming from climate-related events and trends. And conducting one requires the right team.

You’ll want to start by assembling a climate risk assessment steering committee. After securing CEO buy-in, this steering committee will typically consist of the following roles:

- CFO

- Head of Enterprise Risk Management

- General Counsel

- Head of Operations/General Manager

- Head of Procurement/Supply Chain

Beneath this steering committee will sit a task force, comprised of personnel from each of the steering committee’s respective functions as needed. This task force is responsible for conducting the assessment – led predominantly by the risk team – while the steering committee is focused on overseeing, driving forward, reviewing the findings, and reporting to executive leadership and the board of directors.

The team’s first task is to define the company’s business footprint through the physical mapping of business operations, largest suppliers, and business customers. Then determine the physical and transition risks (and level of severity) impacting the organizational footprint.

Physical risks include frequency of weather events like hurricanes, droughts, and wildfires, as well as sea level rise. These risks can be identified through publicly available data (see: IPCC, IEA, WRI), which help organizations understand geographic locations that are most prone to risks.

Transition risks are business-related risks that follow the economic shift toward a low-carbon economy. These are often business model specific and consider the technological, market, legal, regulatory, and reputational risk of the low-carbon economic shift.

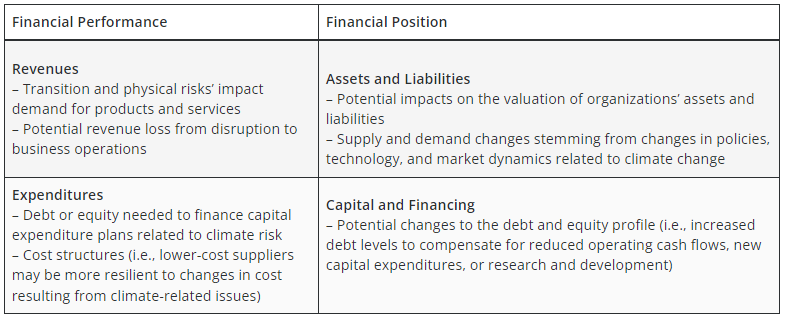

Once an organization categorizes climate-related physical and transition risks, CFOs should then consider actual and potential financial impacts on revenues, expenditures, assets and liabilities, and financing.

2. Start Your Scope 1-2 Emissions Inventory

Collect all data necessary to calculate Scope 1 and 2 emissions based on the GHG Protocol. The Kyoto Protocol recommends calculating emissions for the following seven greenhouse gases: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulfur hexafluoride (SF6). Scope 1 includes direct emissions from stationary and mobile combustion, fugitive emissions. Scope 2 includes indirect emissions from purchased electricity, heating, and steam.

3. Review Scope 3 Emissions

The SEC has proposed that companies disclose Scope 3 emissions and intensity if material, or if the registrant has set a GHG emissions reduction target that includes Scope 3. Although the SEC proposed a number of exemptions related to Scope 3 reporting, a phase-in period, and a safe harbor provision, we believe Scope 3 should be considered and reviewed in the emissions inventory process. To better assess Scope 3 materiality, companies should begin by mapping its value chain to understand where emissions predominantly occur in each of the Scope 3 categories.

4. Risk Management and Oversight

Once you have taken steps 1-3, you can then determine how management and boards can best govern and oversee material climate risks.

A description of management oversight may include:

- The process through which management is informed on climate risk

- Reliance on specific in-house staff or third-party consultants

- Groups responsible for reporting to the board

A description of board-level oversight and governance of climate-related risks may include:

- A description of how the board considers climate risks when reviewing and guiding business strategy and budgeting, as well as how climate risk informs M&A strategy and decision-making

- Acknowledgment of the frequency with which the board is updated on climate risks

If your company has already conducted a thorough climate risk assessment, then your next step is to put together the collective heads of your finance and risk teams and figure out how to translate the findings into a financial impact.

Risk is the name of the game

If you’ve read our bulletin, you know that this proposed rule has a lot of moving pieces to it: Scope emissions tracking, attestation, board oversight, financial quantification, and more. And while each piece is relevant and drives value, they are all peripheral to the overarching issue—climate risk. Climate risk undoubtedly begs CFOs’ attention. Here’s why:

- Regulators are focused on climate risk. Looking at the disclosure requirements within the proposed rule, four of the nine key points are very explicitly focused on exploring or responding to climate risks. And SEC Chair Gensler has said for months that he believes regulated climate risk-focused disclosures are important for establishing consistency in reporting and decision-usefulness for external stakeholders. It seems unlikely, then, that the SEC will abandon its focus on climate risk anytime soon.

- Investors are focused on climate risk. Over the last few years, institutional investors have become increasingly vocal in their advocacy for corporate disclosure of climate risks. This is best exemplified by Larry Fink’s letter to CEOs, in which he says, point blank, “climate risk is investment risk.” In a January 2022 survey of 300 global investors, conducted by CoreData Research for Robeco, 75% of respondents said climate change is a central or significant factor in their investment policy. This is up from 34% two years ago.

- Climate risk is everyone’s problem. The proposed rule, along with reams of sourced literature in the report, will tell you that some elements of climate impact are not applicable for certain companies, including Scope 3 emissions. However, all companies are on the hook for assessing their climate risks—even technology companies that may be perceived as having a smaller footprint. In fact, a recent study published Nature Communications journal looked at the reported GHG emissions of 56 top technology companies. This study found that, on average, these businesses omitted 50% of their total emissions.

- If all else is stripped away, climate risk will remain. It’s no secret that the proposed rule will face tremendous scrutiny. Numerous lawsuits are bound to take place, and with the EPA already regulating “large emitters” there are concerns that the SEC’s rule may step on the toes of the lead environmental agency. Although we can’t definitively know what elements of the rule will remain when all is said and done, we do feel confident that the climate risk element will persist. Both because of its overwhelming relevance to investors and because of its positioning within the Scope of SEC oversight as a driver of financial risk.

Guidance rooted in pragmatism

We understand there are many publications with just as many recommendations on what to do next—most of which involve huge undertakings that add complexity to the process. As we look pragmatically at the future of the proposed SEC rule, the most important information for investors, and the biggest value drivers for CFOs, all signs point to the climate risk assessment.

If you’re unsure on just how to get this initiative off the ground, are uncertain about your teams’ capabilities, or simply want support along the way, reach out to us. We’re happy to assist in the climate risk assessment process, as well as the many critical pieces that come afterward.

Want to get additional insights direct to your inbox?

Subscribe to Riveron Insights and get relevant news and trends shaping the world of finance, accounting, and operations.