This month, Riveron sponsored and presented at the 42nd Annual SEC and Financial Reporting Conference hosted by the University of Southern California Leventhal School of Accounting and the Financial Executives Institute (FEI).

The conference themes spanned materiality, evolving standards, internal controls over financial reporting, and more. Riveron experts have compiled key takeaways from the conference that will be relevant for accounting and finance professionals preparing for their companies’ quarterly and annual reporting.

In addition to Riveron’s presentation on artificial intelligence for CFOs and controllers, the conference featured insights from accounting industry leaders. These included the US Securities and Exchange Commission (SEC) staff, members of the Financial Accounting Standards Board (FASB), Fortune 100 finance and accounting executives, and representatives from the top national accounting firms.

The gathering provided an excellent opportunity to hear from accounting leaders on the latest themes emerging from busy season as companies refine their financial reporting practices and look toward preparing for year end. Here are the important conference takeaways for the office of the CFO:

Risk assessments, in-progress projects, and other topics explored at the SEC and FASB leaders’ fireside chat

The conference began with a fireside chat featuring the SEC Chief Accountant Paul Munter and FASB Chair Rich Jones. Both leaders reiterated themes they had previously highlighted at the 2023 SEC conference.

Munter discussed several statements issued by his office, addressing various practice issues from rigor in the statement of cash flows to the tone at the top of accounting firms. He emphasized that the accounting profession must prioritize quality financial reporting, integrity, and professionalism over growth.

Specifically, Munter highlighted the importance of financial statement preparers and auditors performing a quality risk assessment. He commented that, in some circumstances, the risk assessment process is too focused on a narrow scope of information while not considering broader economic circumstances that may impact the analysis. A holistic risk assessment should consider the activities and results of companies and examine the dynamic environment in which they operate.

Rich Jones, the FASB Chair, highlighted the current FASB agenda. He noted that, upon assuming his role, the FASB conducted an outreach effort to identify topics relevant to investors and preparers, ensuring that the FASB agenda output benefits investors. Jones also mentioned the reconstituted Emerging Issues Task Force (EITF), which addresses practice issues more swiftly and integrates them into the FASB agenda with suggested solutions.

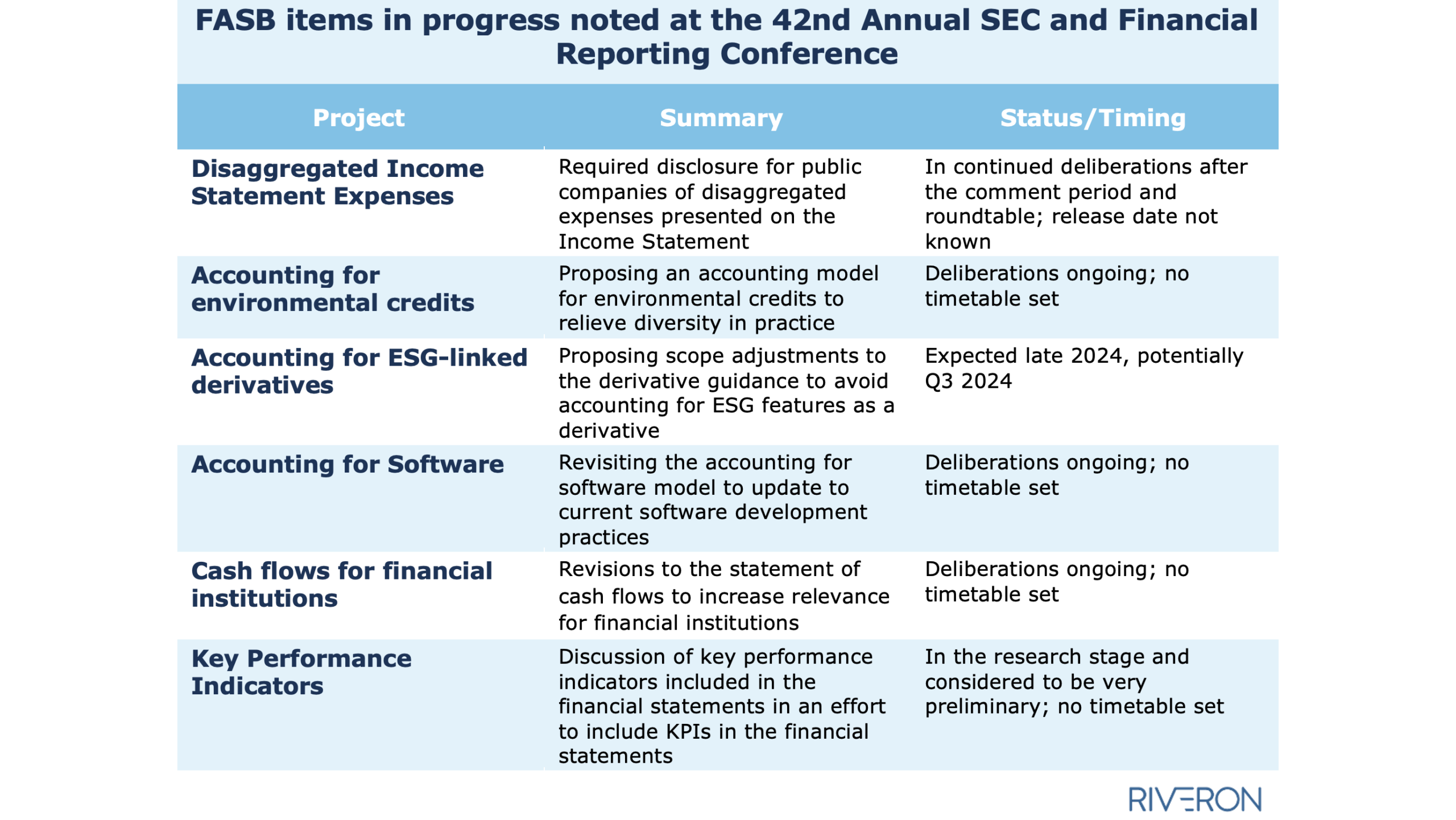

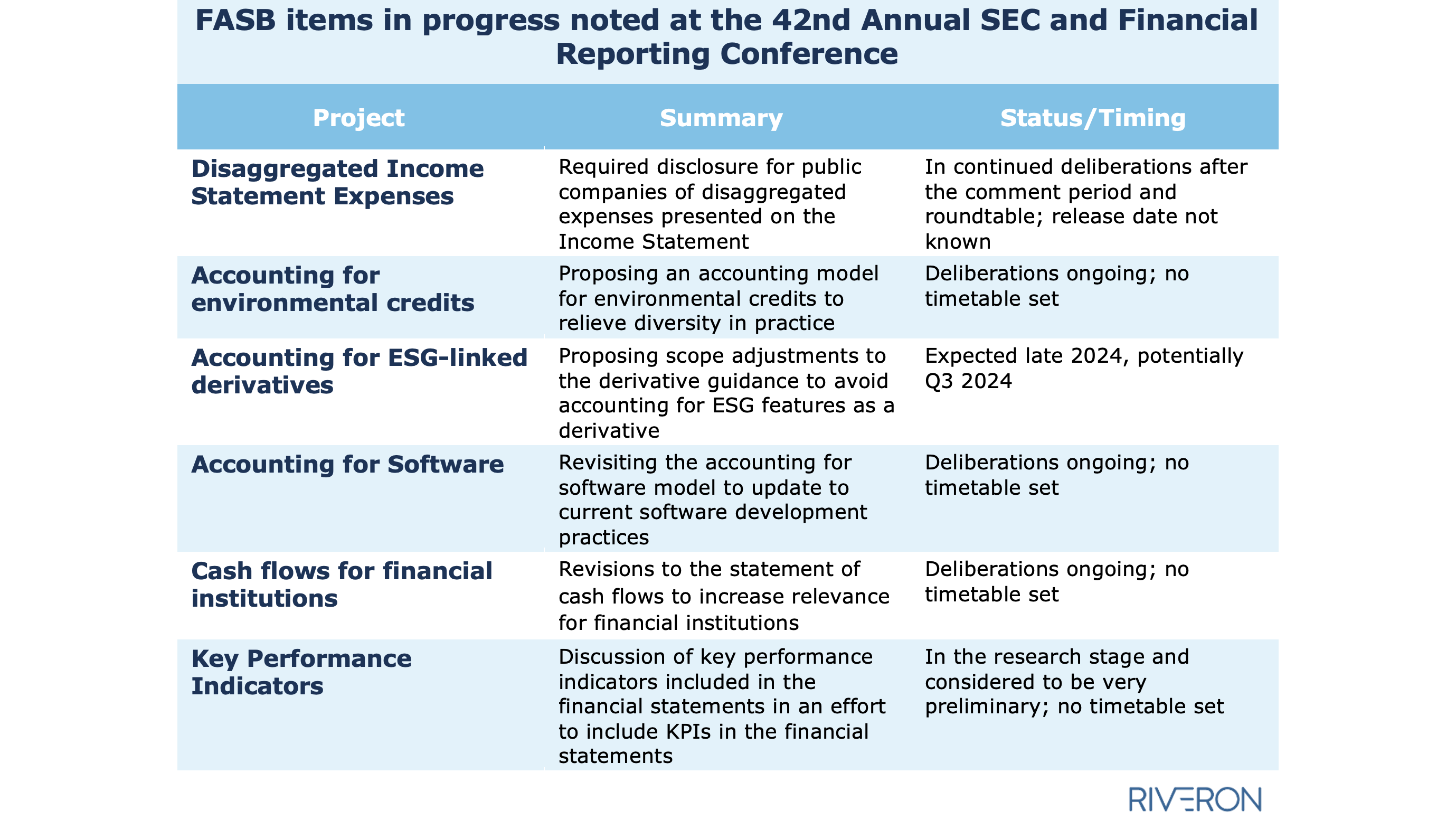

Jones outlined several projects in progress, including the following:

Jones also highlighted several recently issued standards, including the standard on digital assets, as an example of how the FASB continues to look for ways to be responsive to industry demands.

Current practice takeaways included materiality, data, and internal controls

Beyond the presentations from the SEC Chief Accountant and FASB Chair, the attendees heard from a panel of accounting firm leaders regarding current practice and audit issues, a controllership panel, and from the SEC Chief Accountant of the Enforcement Division. The presentations covered a variety of topics and concerns in current practice. Topics of note throughout the day included:

Materiality: From cybersecurity to climate disclosures to the evaluation of a misstatement, a thorough and objective assessment and documentation of materiality is critical. In certain areas such as cybersecurity and climate disclosures, defining materiality is a novel concept and will take significant work with key stakeholders outside of the financial reporting department. When it comes to the financial statements, there continues to be significant SEC focus on the evaluation of materiality with regards to evaluation of a misstatement utilizing the guidance in SAB 99. The staff underscored that these assessments should not be viewed as something that a company can simply “document their way out of” but require objective assessments of quantitative and qualitative factors, if relevant.

Data Management and Systems: While the conference did not dwell on the general shortage of accounting talent, it did highlight strategies to cope with these shortages. One key strategy is the implementation of robust data management practices. Effective data management contributes to reliable financial reporting and helps mitigate the impact of talent shortages. For instance, Riveron led a discussion on AI in Accounting that explored various use cases beyond large language models, focusing on automating processes and enhancing data validation. The controller roundtable further emphasized the importance of systems that manage data effectively and the need for financial reporting teams to rigorously validate that data. Good data practices are essential for ensuring the accuracy and reliability of financial reports, especially in an environment where accounting resources are stretched thin.

Internal Controls over Financial Reporting: Internal controls over financial reporting (ICFR) was a major focus throughout the panels, highlighting several key problem areas:

- Sufficient Personnel and Expertise: Ensuring teams have the right personnel with the necessary expertise is crucial, particularly amid current talent shortages.

- Adequate Resources: Sufficient resources, including access to technology and AI, are essential to support robust internal controls.

- Information Flow: Critical information must reach the appropriate individuals for informed decision-making.

- Integration of Acquired Systems: Effective controls are necessary to ensure accurate financial data during system integrations.

- Cybersecurity Disclosures: Accurate and timely disclosures are vital in the face of increasing cyber threats.

- Risk Factor Disclosures: Properly identifying and disclosing risk factors is essential for transparent financial reporting.

Preparers should consider the total communication to investors, beyond just the audited financials and footnotes. Investing in ICFR and disclosure controls and procedures (DCP) can help identify problems early, leading to better reporting and fewer issues escalating to the division of enforcement.

Recurring conference topics relevant for the office of the CFO

In addition to the key themes noted above, the conference participants briefly mentioned several topics that often arise at these events. The office of the CFO should continue to monitor these topics throughout the year to ensure accounting and financial reporting practices are aligned to the latest guidance.

SEC comment letter trends are a common subject closely followed by preparers, and the following topics were highlighted during the conference:

Emerging areas of comments, including:

- Inflation and interest rates

- Supply chain

- Regional matters related to Ukraine, China, and Israel

- Impairment

- Climate-related disclosures

- Human capital

- Cybersecurity

- Digital Assets (Crypto)

“Evergreen” topics that continue to be a focus:

- Non-GAAP measures

- MD&A

- Revenue recognition

- Business combinations

- Segment reporting

- Inventory and cost of sales

- Critical accounting estimates

- Disclosure controls and ICFR

Additionally, the Division of Corporate Finance indicated other trending consultation topics, which included:

- New SEC clawback rules and the use of the cover page checkboxes

- New segment reporting guidance and the application of the guidance to Non-GAAP measures

- Cybersecurity breaches and 8-K disclosures

Overall, the 42nd Annual SEC and Financial Reporting Conference offered valuable insights from key regulators, standard-setters, and industry leaders. While some topics remain consistent, the focus on emerging issues highlights the ever-evolving financial reporting landscape. Companies must stay vigilant and proactive in their reporting practices to navigate these changes effectively.

Need guidance related to accounting and financial reporting?

Riveron supports the office of the CFO in navigating today’s multifaceted challenges and equips accounting and finance teams to make strides before, during, and after the demands of audit season.

Through our technical accounting experience and cross-functional expertise, Riveron helps CFOs optimize accounting and finance resources, manage risks, and adapt to change. To learn more, connect with an expert today.

Connect with an Expert