Executive Summary

This brief outlines California’s Climate Accountability Package, which includes SB 253 and SB 261, requiring companies to disclose carbon emissions and climate-related financial risks. The California Air Resources Board (CARB) is expected to finalize regulations at the end of 2025.

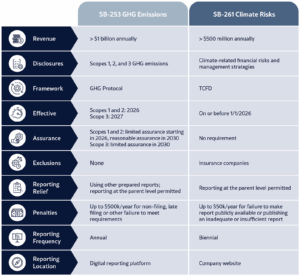

- SB 253 requirements: Companies must annually disclose Scope 1, 2, and 3 greenhouse gas emissions, following the Greenhouse Gas Protocol standards. Initial reports for Scope 1 and 2 are due in 2026, with Scope 3 expected in 2027.

- SB 261 requirements: Companies are mandated to report biennially on climate-related financial risks, aligned with the Task Force on Climate-Related Financial Disclosures (TCFD). The first report is due by January 1, 2026.

- Assurance requirements: Limited assurance will be required for Scope 1 and 2 emissions in the first reporting year, transitioning to reasonable assurance by 2030. No assurance is needed for climate risk disclosures under SB 261.

- Enforcement and penalties: Non-compliance penalties can reach up to $500,000 for SB 253 and $50,000 for SB 261 per year. CARB will exercise enforcement discretion during the initial reporting cycle for good faith efforts.

- Future implications: Other states are considering similar legislation, and California’s requirements may influence national and international climate reporting standards.

- Support from Riveron: Riveron can help companies prepare for compliance through data management, climate risk assessments, emissions calculations, and assurance readiness.

Disclosures

SB 253: The Climate Corporate Data Accountability Act

SB 253 mandates the reporting of scope 1, 2, and 3 emissions.

- Scope 1 includes the direct emissions produced from the reporting company’s operations, such as company-owned vehicles, on-site power generation, and fuel combustion.

- Scope 2 includes indirect emissions from energy purchased by the company, such as electricity from electric utilities.

- Scope 3 is value chain emissions associated with the company’s upstream and downstream activities.

Emissions for each category must follow the data collection and calculation standards established by the Greenhouse Gas Protocol (GHG Protocol) for corporate use. The GHG Protocol provides guidelines for measuring and reporting emissions from a company’s direct operations and value chain and has a specific standard for each scope of emissions.

The current draft of the regulation requires scope 1 and 2 emissions to be reported first in 2026, with scope 3 disclosures to follow, likely in 2027. The inventory must be based on data from the prior fiscal year; therefore, companies should begin thinking now about how to approach 2025 data collection if they have not already done so.

SB 219 requires CARB to adopt regulations governing the disclosure of these emissions, including setting reporting timelines for scope 1, 2, and 3 emissions. It also allows consolidated reporting at the parent company level. CARB’s final rulemaking decision is expected by the end of 2025.

SB 261: The Climate-Related Financial Risk Ask

SB 261 requires companies to report biennially on relevant climate-related financial risks and subsequent management measures. The rule requires companies to report their climate risk process in accordance with the Task Force on Climate-Related Financial Disclosures (TCFD). TCFD utilizes four pillars for disclosure: Governance, Strategy, Risk Management, and Metrics & Targets. The first disclosure is due by January 1, 2026.

Companies can disclose the information required by both SB 253 and SB 261 either in a standalone report on their website or within a broader sustainability report, without needing to include it in annual filings. Furthermore, SB 253 mandates the disclosure of GHG emissions through a digital reporting platform that CARB is responsible for developing. CARB is expected to provide more details regarding the specifications and functionality of this digital repository.

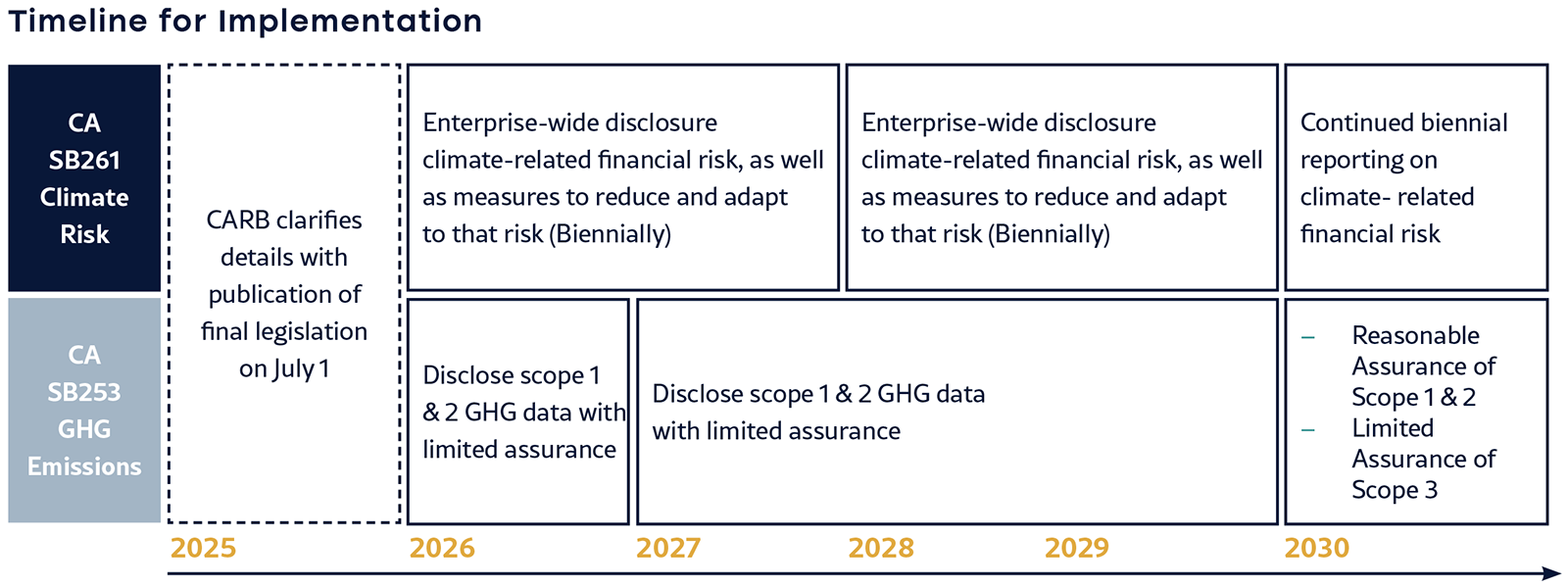

Timeline for Implementation

2026:

- January 1, 2026 – SB 261 Climate Risk disclosure. The climate-related financial risks report must be posted on a company’s website by January 1st, 2026. After that, the report must be updated every two years. CARB is expected to clarify if there will be a set reporting period or if companies may use their own fiscal year or ERM timeline.

- TBD – Scope 1 and 2 emissions are due in 2026, based on prior year (FY2025) data. CARB is expected to clarify the filing date within 2026, from which GHG emissions will need to be reported, and define the reporting period. When setting the deadlines, CARB is expected to consider typical emissions data aggregation timelines and the ability to conduct independent assurance.

2027:

- TBD – Reporting Scope 3 emissions will be addressed later, likely in 2027, based on FY2026 data. The initial proposed legislation stipulated that scope 3 data must be disclosed 180 days after the disclosure of scope 1 and 2 data became public. However, that has since been walked back, and instead, CARB will clarify the scope 3 reporting timeline by the end of 2025.

Assurance Requirements

- Scope 1 and 2 will first require limited assurance over 2025 data in the first reporting year, a less rigorous standard than reasonable assurance. With limited assurance, an independent auditor performs substantially less extensive procedures than a full audit. The goal is to seek an acceptable level of comfort, primarily through inquiry and analytical procedures, so there are no significant mistakes, meaning the disclosures are generally satisfactory and don’t have any big, potentially misleading errors. This process does not result in the auditor expressing an opinion.

- After their review, the independent auditor will issue a formal written report containing specific elements, including their conclusion. Based on their review, the auditor will state whether they are aware of any material modification needed for the disclosure to align with the rules for the Company’s claims to be accurate. Limited assurance aims to credibly support the emissions disclosures but recognizes the limitations in the scope of work performed.

- In 2030, scope 1 and 2 will be required to achieve reasonable assurance, and scope 3 data will be required to achieve limited assurance. Currently, there is no proposal to require reasonable assurance over scope 3 data.

- No assurance is required for the climate risk disclosures under SB 261.

Enforcement and Monitoring

- The original bill stipulated non-compliance penalties of up to $500,000 for SB-253 and $50,000 for SB-261 per reporting year. Specifically, for scope 3, any penalties assessed between 2027 and 2030 on scope 3 reporting would be for non-filing.

- On December 5, CARB announced in a notice that it would exercise enforcement discretion for the first reporting cycle, on the condition that entities demonstrate good faith efforts to comply with the requirements of the law.

- This enforcement update aims to support companies actively working towards compliance. CARB acknowledged that companies may require time to set up new data collection methods for comprehensive scope 1 and 2 reporting if they don’t already have or gather this data.

- Therefore, for the initial reporting period, CARB will not penalize companies for incomplete reporting if they demonstrate a reasonable effort to keep all data related to their prior fiscal year’s emissions.

- CARB is expected to provide details about reporting for later years as part of their ongoing rulemaking process.

What to expect next: Clarification from CARB

Since the initial legislation was proposed, several changes to the rules have been enacted. The comment period ended on March 21, 2025, and the California Air Resources Board (CARB) will publish the final legislation by the end of 2025.

- A few amendments have already been introduced:

- Allow companies to consolidate reporting at the parent level

- Removed the requirement for companies to pay a filing fee at the time of disclosure

- For the first disclosure cycle, CARB will exercise enforcement discretion, meaning companies that it views as making good-faith efforts towards compliance may not be penalized

- There are several details in the rule expected to receive further clarification:

- Definition of “doing business” in California

- CARB’s enforcement methods and the penalty for non-compliance

- Standardization of reporting period, to account for different companies’ fiscal year ends

- Clarification on whether SB 261 will impose more prescriptive requirements for quantitative analysis and reporting (i.e., requiring climate scenario analysis or a threshold for financial impacts).

- Exact reporting deadlines for scope 1, 2, and 3 emissions under SB 253

Additional Climate Reporting Requirements are Coming

The introduction of this legislation has had ripple effects outside of California. For many companies in the United States, climate reporting requirements focused on GHG emissions and climate-related risks is going to impact them.

- To date, 5 other states have announced plans to introduce similar legislation. These states – New York, Washington, Colorado, Illinois, and New Jersey – have either cited the California legislation as the catalyst for their own rule-making or expressed a desire to adopt a replica of the California law.

- Outside the US, this legislation overlaps with other reporting requirements, such as the CSRD in the EU.

- This week, California proposed another bill, SB 755, that would expand climate reporting requirements to include large state contractors. The requirements would likely align with those in SB 253 and 261.

How Riveron Can Help Companies Prepare

Riveron’s integrated expertise in climate, regulatory compliance, and accounting advisory delivers comprehensive sustainability solutions. We provide end-to-end support, from data collection to disclosure, by building reliable processes that ensure data accuracy and compliance.

- Source, aggregate, and manage data: To meet the 2026 reporting deadlines, companies must collect and organize data for calculations immediately. The first meaningful step towards compliance, sourcing unstructured and disparate data, is often a complex challenge. Riveron’s unique combination of sustainability and accounting expertise streamlines this process, clarifying the scope of data collection and ensuring the accuracy of audit-ready data.

- Conduct a climate risk assessment: Leveraging our proprietary tool, our climate experts provide comprehensive climate risk assessments. We deliver customized risk registers, integrate climate considerations into your ERM, and generate TCFD-aligned disclosures, ensuring thorough evaluation of operational and financial impacts.

- Calculate Scope 1, 2, and 3 emissions: To ensure accurate calculation of Scope 1, 2, and 3 emissions, our team leverages its climate expertise, proprietary tools, and robust methodologies. We manage the entire process, from defining organizational boundaries and mapping value chains to collection, calculation, and quality checks. We work closely with our clients to deliver comprehensive emissions reports, ensuring compliance with all relevant regulatory requirements, including California SB-253.

- Establish internal controls: Our integrated team, which includes former auditors, provides a rigorous approach to enhancing your confidence in your sustainability data. We assess, plan, and execute process walkthroughs to identify and remediate control gaps, ensuring the accuracy and completeness of data. Our approach to internal controls delivers a strong foundation for reliable sustainability reporting.

- Prepare for assurance: Riveron leverages its deep regulatory reporting and audit experience to deliver exceptional assurance readiness for sustainability disclosures. We streamline the preparation process, expertly manage auditor interactions, and reduce the strain on your team. Our partnership ensures a faster assurance timeline, superior data quality for review, and seamless compliance. We bring clarity and control to the assurance process.

- Implement technology to streamline reporting: Riveron leverages technology to ensure accurate and efficient ESG data collection and analysis, directly addressing compliance and stakeholder reporting requirements. We collaborate with business and technology leaders to implement digital solutions that significantly reduce the reporting burden on finance, accounting, and other teams. By automating and streamlining the reporting process, Riveron empowers these teams to focus on core responsibilities while delivering transparent and reliable sustainability information. We partner with technology solutions that simplify ESG reporting, enhancing accuracy and freeing up valuable resources.

Connect with an Expert

Need guidance related to climate disclosure updates?

Our team partners with the office of the CFO and other accounting stakeholders to simplify complexities and address your team’s most pressing needs.