US Commercial Real Estate Trends and Tax Impacts for Foreign Investors

A longstanding tax act, FIRPTA, continues to impact the current decisions and the potential value realized by foreign investors of US real estate.

A version of this article first appeared in Commercial Property Executive; partial excerpts are provided below.

As leaders navigate the ups and downs of today’s business climate, the US commercial real estate market’s instability may lead to more distressed sales, deleveraging, or portfolio adjustments. For foreign investors considering any of these transactions within the United States, it’s important to understand the current impacts of the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA). This decades-old law covers US federal income tax implications that are still relevant today but might be overlooked by foreign investors. FIRPTA requires US tax withholding and compliance from foreign investors, and dealing with these tax matters can be complicated and burdensome for companies and investors alike.

When exploring tax considerations, withholding exemptions, and the nuances of selling, it can be beneficial for real estate investors to work with a tax advisor to tailor strategies supported by an informed understanding of FIRPTA.

When foreign investors owe taxes on US real-estate gains

Foreign investors are generally not taxed on gains from the sale of capital assets — unless that gain is effectively connected to a US trade or business. As a result, a foreign investor can sell shares of a US corporation without being taxed on the gain. Regarding real estate assets, FIRPTA overrides this general rule to treat a gain or loss on the disposition of a US Real Property Interest (USRPI) as effectively connected income — which is subject to US tax. As such, foreign investors who hold USRPIs would be subject to US federal income tax at the appropriate US income tax rate. This would include foreign corporations, which would be subject to tax at 21 percent.

Further, FIRPTA imposes a 15 percent withholding tax on any foreign seller of US real estate, and the withholding obligation falls on the buyer of the real estate. Generally, tax treaty benefits may apply to reduce the rate of withholding. The withholding is assessed on total proceeds (rather than on the sale’s net gain), which will reduce after-tax cash flows. If a foreign investor overpays the withholding tax, they can file a US tax return to claim a refund from the Internal Revenue Service (IRS). It is important to note that a FIRPTA presumption applies to treat all US corporations as US Real Property Holding Companies (USRPHCs) unless documented otherwise.

Real estate assets or stocks subject to FIRPTA

Under FIRPTA, US Real Property Interest is a key consideration. USRPI is broadly defined as any direct interest in real property located in the United States or the Virgin Islands, including fee ownership, leaseholds, or options to acquire fee or leasehold ownership, as well as land improvements, and any associated personal property. The Internal Revenue Code further assigns the USRPI designation to include an interest, other than as a creditor, in any US corporation which is determined to be a US Real Property Holding Company (USRPHC). Note that a five-year lookback would apply to any USRPHC determination.

A USRPHC is any corporation where the fair market value of its USRPIs is at least equal to 50 percent of the sum of the fair market values of the corporation’s USRPIs, foreign interests in real property, and other assets used or held for use in a trade or business. Thus, the sale of stock in a domestic corporation heavily invested in US real estate would be subject to FIRPTA.

Generally, any foreign investor holding stock in a publicly listed US company is exempt from FIRPTA unless the investor holds more than five percent of the outstanding shares of the company or the company meets the definition of a Real Estate Investment Trust or Regulated Investment Company.

The FIRPTA rules also apply to corporate liquidations of any USRPHCs. Generally, corporate liquidations involve the exchange of stock for the liquidating corporation’s assets. As a result, liquidation can be considered a disposition of a USRPI.

For additional details, read the full original article at Commercial Property Executive.

Withholding tax exemption

Section 1445 requires transferees of USRPIs, including USRPHCs, to withhold 15 percent of the amount realized on a disposition by a foreign person. As noted, tax treaty benefits may apply. Exemptions to withholding require the foreign investor to provide documentation about its tax status to the transferee. Meeting these requirements is crucial to obtaining the exemption and, therefore, proper deal execution.

US real estate deal considerations

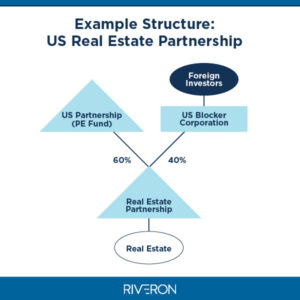

A common example of a simple US real estate partnership structure is as follows:

In the above structure, US investors, such as private equity funds and other institutional investors, own an indirect interest in a Real Estate Partnership through a US partnership intermediary. Foreign investors — which could be corporations, partnerships, or individuals — typically own an indirect interest in the Real Estate Partnership through a US blocker corporation. The Real Estate Partnership invests and manages the real estate portfolio.

For instance, assume that the Foreign Investors own 100 percent of the US Blocker Corporation, the US Partnership owns 60 percent of the Real Estate Partnership, and the US Blocker Corporation owns 40 percent. Also assume that the Real Estate Partnership is 100 percent invested in US real property interests.

Under Section 897(c)(4)(B), the US Blocker would be treated as owning its share of the Real Estate Partnership’s USRPI. Since the US Blocker has no other activity, 100 percent of its assets are classified as USRPIs, and as such it is likely to be treated as a USRPHC.

As the US Blocker is subject to US federal income tax, FIRPTA would not apply to its allocation of gains or losses from the Real Estate Partnership.

If, on the other hand, the foreign investor sold its shares in the US Blocker, this transaction would be subject to FIRPTA. The transferee or withholding agent would request documentation to exempt US Blocker from withholding, or reduce withholding, if applicable, on the foreign investor.

How the structure impacts selling

When planning to exit, it’s important to consider the legal structure. The outcome may vary based on the chosen exit approach:

- A direct disposition of the US Blocker that could be considered a disposition of a USRPHC and subject to 15 percent withholding and related filing requirements with the IRS.

- A sale of property by Real Estate Partnership, could create gain or loss allocated to the US Blocker. A subsequent distribution of sale proceeds to the US Blocker would reduce US Blocker’s outside basis in Real Estate Partnership; however, due to US Blocker’s status as a US corporation, FIRPTA withholding would not apply.

- A sale or redemption of the US Blocker’s interest in the Real Estate Partnership would be recognized and taxed at the US Blocker. No FIRPTA consequences would result, as the US Blocker has recognized the gain from the disposition of the USRPI.

Exiting investments in US real estate can be complicated. All parties involved should seek guidance and assistance from experienced tax advisors who can help investors understand the necessary steps and provide recommendations for the transaction.

Need help with tax advisory?

Whether your team is navigating year-end cycles, strategic adjustments to a real estate portfolio, or other tax advisory needs, Riveron’s cross-functional team of experts is here to help. We partner with our clients and their stakeholders to elevate performance and expand possibilities across the transaction and business lifecycle. Contact us to learn more.