E&S Metrics In Executive Compensation: What Do Investors Really Care About?

The investor landscape around E&S metrics in executive compensation programs is quickly evolving as institutions are pressured to set stricter, and more public, policies covering this formerly niche area, rating agencies are increasingly reporting on the use of E&S compensation metrics, and there are a growing number of shareholder resolutions requesting the adoption and disclosure of E&S compensation metrics.

Companies will need to enhance disclosure of E&S compensation metrics in executive incentive programs in next year’s proxy, and better show how executives are compensated against ESG goals, not simply financial performance.

E&S-remuneration shareholder resolutions increase despite overall decrease in shareholder activism

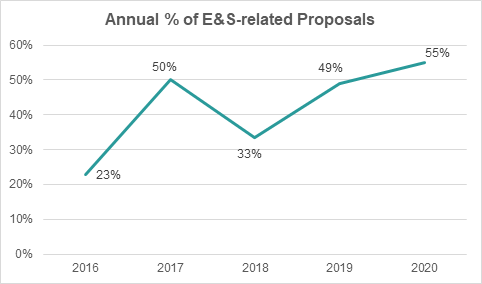

In the past five years, the percentage of E&S-related remuneration shareholder proposals (relative to all remuneration shareholder proposals) for U.S. corporate issuers has steadily increased. An E&S-related remuneration shareholder resolution is defined as a shareholder resolution calling for an amendment to, or increased disclosure around, an existing executive compensation program that specifically references an environmental or social goal.

In 2016, 23% of remuneration shareholder proposals were E&S-related, whereas in 2020 thus far 55% of remuneration shareholder proposals have been E&S-related. In the first half of 2020 alone, E&S-related remuneration shareholder proposals increased roughly 600 basis points relative to total remuneration proposals from full year 2019. This steady increase in E&S related remuneration proposals in 2020 thus far, amidst an overall decrease in shareholder activism, signals continued investor interest in ESG metrics in executive compensation programs.

Support for these proposals has steadily grown as well, averaging a 23% approval rate in 2019, with some such as a proposal to Oracle on gender pay reporting garnering as much as 36% support from shareholders.

Source: ProxyInsight

Source: ProxyInsight

ESG Ratings Report on the “E&S” and “G” Components of Executive Compensation

Rating agencies and proxy advisors have traditionally captured the governance (“G”) component of executive compensation by reporting on responsible allocation of capital, use of equity, pay-for-performance alignment, and pay transparency measures. More recently, rating agencies have begun to evaluate the “E” and “S” component of executive compensation by reporting on the use of sustainability metrics in incentive programs.

As companies look to improve their ESG scores with rating agencies and build out more robust ESG programs, one way to assure investors that your company is proactively managing ESG risks and opportunities, is to include E&S performance metrics in executive pay. Companies should review specific ESG goals they have shared with investors in the past and include quantitative and qualitative targets in the executive compensation package that measure the advancement of those sustainability initiatives and commitments.

Below is a list of factors that ESG rating providers evaluate with regards to the “E&S” and “G” components of executive compensation.

MSCI ESG Rating

According to the MSCI ESG Ratings Methodology, the following metrics are considered when evaluating executive compensation programs:

Compensation-related E&S factors:

- Has the company, if designated as having either a high environmental or social impact, failed to incorporate links to sustainability performance in its current incentive pay policies?

- High Environmental Impact: If any of the following ESG Ratings Key Issues carry more than a 5% weight: Carbon Emissions, Water Stress, Toxic Emissions & Waste, Product Carbon Footprint, Raw Material Sourcing, Packaging Material & Waste, Electronic Waste, Biodiversity & Land Use, Energy Efficiency.

- High Social Impact: If any of the following ESG Ratings Key Issues carry more than a 5% weight: Labor Management, Health & Safety, Product Safety & Quality, Supply Chain Labor Standards, Human Capital Development.

- In an effort to reduce exposure through comprehensive Health & Safety policies and implementation mechanisms, does the company include H&S as a factor in determining executive compensation?

Compensation-related factors:

- Does the CEO hold shares with a value below 5x salary and has the company failed to adopt either effective stock ownership guidelines or an equity retention policy for the CEO?

- Has the number of shares held by the CEO (after adjustment for any corporate actions) decreased year over year by 10% or more?

- Does the CEO’s equity pay fail to reflect the company’s total shareholder return (TSR) performance over the last three and five years?

- Does the CEO’s equity pay fail to reflect the company’s TSR performance over the last three and five years relative to his or her Pay Peer Group?

- Did the CEO’s annual incentives fail to rise or fall in line with annual performance for the last reported period?

- Where the company offers variable or incentive pay, has the company failed to adopt a clawback policy, applicable to both the annual and long-term incentives, that would recoup incentive pay based on accounts that were restated at a later date?

- Has the company provided a golden hello to its CEO or other senior executives?

- Have the company’s pay policies or practices attracted adverse public comment from stakeholders (including shareholders, government, regulators, etc.)?

- For the most recently reported period, did the company receive a negative vote in excess of 10% on its pay policies and practices?

S&P Global ESG Scores

According to the SAM Corporate Sustainability Assessment (CSA), the following metrics are considered when evaluating executive compensation programs:

Compensation-related E&S factors:

- Does your company provide incentives for the management of climate change issues, including the attainment of targets?

- What is the ratio of average female to male salary at the executive, management, and non-management level?

Compensation-related factors:

- Does your company have predefined financial returns and/or relative financial metrics relevant for Chief Executive Officer’s variable compensation?

- Does your company have the following compensation structures in place to align with long-term performance? Deferral of Bonus for Short-term CEO Compensation?

- What is the longest performance period applied to evaluate variable compensation covered in your executive compensation plan?

- Is there a clawback policy in place?

ISS Governance and Environmental & Social QualityScore

According to the ISS Governance QualityScore and Environmental & Social QualityScore Methodology Guide, the following metrics are considered when evaluating executive compensation programs:

Compensation-related E&S factors:

- Does the company provide information indicating a link between consideration of ESG risks and performance, and executive remuneration?

- Does the company disclose specific non-financial targets in executive compensation plans?

- Does the company indicate that strategic ESG-related key performance indicators (KPIs) in the company plan are represented in the compensation or remuneration metrics?

- Does the compensation policy explicitly reference specific science-based targets for reducing GHG emissions with a reference to the 2°C scenario?

- Has the company explained how the variable pay award, dependent on non-financial performance, was assessed for the year under review?

- If the company suffered a major controversy, is any increase in salary or bonus proposed for the directors employed at the time of the incident?

Compensation-related factors:

- What is the level of disclosure on performance measures for the short-term incentive plan for executives?

- What is the holding or retention period for stock options and restricted shares or stock awards for executives?

- What percentage of the salary is subject to stock ownership requirements or guidelines for the CEO?

- Did the company disclose a clawback or malus provision?

- What is the multiple of pay in the change-in-control or the severance agreements for the CEO?

- Does the company provide excise tax gross-ups for change-in-control payments?

- What is the size of the CEO’s one-year pay as a multiple of the median pay for the company’s peers (MOM)?

- What is the degree of alignment between the company’s TSR and change in CEO pay over the past five years (PTA)?

- What is the ratio of the CEO’s total compensation to the next highest paid executive?

- Does the company have a robust policy prohibiting hedging of company shares by employees?

- What is the level of disclosure on performance measures for long-term equity and cash awards granted in the last fiscal year?

- What is the basis for the change-in-control or severance payment for the CEO?

- Has the ISS qualitative review identified a pay-for-performance misalignment?

- Has ISS identified a problematic pay practice or policy that raise concerns?

Sustainalytics

According to the 2019 Sustainalytics Indicators ESG Risk Ratings Overview, the ESG Performance Targets indicator evaluates whether part of executive remuneration is explicitly linked to sustainability performance targets, such as health and safety targets, environmental targets, or diversity. If executive remuneration is tied to some of these ESG-related factors, Sustainalytics believes this indicates executive-level responsibility for promoting the initiative.

Sustainalytics assesses the following areas:

- Remuneration Disclosure

- Remuneration Committee Effectiveness

- Say on Pay

- Pay Controversies

- STI Performance Matrices and LTI Performance Matrices

- Disclosing qualitative and quantitative targets

- Strong pay-for-performance links

- LTI is subject to pre-set goals for performance over a period of set time and specific quantifiable performance metrics with pre-set targets are disclosed for performance-based components of the LTI

- Pay Magnitude

- Pay for Performance

- Pay for Failure

- CEO Termination Scenarios

- Internal Pay Equity

- Clawback Policy

Industry and market-cap insight

Although the use of ESG metrics in executive compensation programs is not currently a mainstream practice, many large-cap and multi-national companies across a range of industries have begun to integrate sustainability metrics into executive compensation programs. This practice tends to focus on short-term incentive programs, and includes multi-national companies such as Royal Dutch Shell, Intel, Alcoa, PepsiCo, and Mead Johnson, to name few.

Based on our research, we found that no one industry leads in adopting ESG compensation metrics, and that E&S metrics vary greatly based on industry.

Retail companies adopting ESG metrics in executive compensation programs tended to focus on social factors such as corporate culture and diversity. For example, Kohl’s evaluates CEO performance based on several performance objectives, 10% of which takes into account the progress achieved in “enhancing Company diversity, and social responsibility”. Gap Inc. uses a performance culture and corporate objectives component as part of its annual incentive package.

Oil & gas companies typically provide more general, non-quantitative sustainability targets. For example, Diamondback Energy, Inc. and SM Energy Company added ESG performance factors into their short-term annual cash incentive award plans, but did not specify the target metric goals. Diamondback requires its executives to meet or exceed key environmental and safety metrics “including flaring, GHG emissions, recycled water, reportable oil spills and Total Recordable Incident Rate (safety)” while SM Energy links executive compensation to a “mix of financial, operational, and ESG-based metrics over time.”

According to recent report by Sustainalytics, materials, energy and utilities sectors accounted for the bulk of the OH&S compensation metrics (The state of pay: executive remuneration & ESG metrics, pg. 3, Exhibit 3: Number of FTSE AW firms with OH&S pay-links by sector). For example, Tronox Holdings plc., a specialty chemicals company, ties 16% of their NEOs’ salaries to safety performance, through metrics such as the disabling injury frequency rate and the total recordable injury frequency rate.

When it comes to market-cap, ESG-related compensation metrics were more commonly adopted by large and mid-market cap companies, such as General Motors, Freeport-McMoRan and Wynn Resorts. Given that large and mid-market cap companies often tend to have more company resources to dedicate to sustainability programs and have larger shareholder bases, which increases the likelihood that they have a larger number of shareholders who value ESG, it does not come as a shock that these companies are leading the way. That said, however, small market-cap companies, such as SM Energy Company, continue to adopt ESG metrics into executive compensation programs, reflecting the importance of ESG incentives and oversight for companies of all sizes.

Aligning a company’s ESG performance with executive compensation is likely to become more of a focal point for investors in coming years. Companies should continue to keep this on their radar as a near-term item to consider across sectors and market caps. Companies interested in aligning ESG strategy with compensation strategy, should first define the key performance indicators (KPIs) used to track and measure company-specific ESG goals, and then clearly disclose these KPIs in ongoing investor communications. Investors are most interested in how your company defines the unique ESG risks and opportunities specific to your business.