Passive investing is nothing new. And it’s in no way a fringe concept. Since its inception 50 years ago, the investment style has been steadily on the rise. As a $16 trillion industry today, passive investing is now double the size of the private equity, venture capital, and hedge fund industries combined.

Still, many corporate issuers—even those that are heavily passively-owned—struggle to understand the mechanisms of passive investing and what it all means for their businesses in general, and their IR strategies in particular. To shed some light on the topic and answer the questions most commonly posed by companies, Riveron dug into the data. Here’s what we learned, what you need to know, and what you can proactively do to make the most of every passive investment dollar in your business.

Answers to 5 critical passive investing questions

1. What is passive investing?

- Broadly defined, passive investing is an investment style that’s typically benchmarked to an index or exchange-traded fund (ETF). Of the 5,000 largest passively managed funds, 94% are truly index-based, meaning they track either a custom or existing benchmark, such as the S&P 500. The returns of the fund should mirror the returns of the benchmarked index.

- The biggest difference compared to active investing is that passive fund managers are minimally engaged over the lifecycle of their investments. In other words, passive fund managers are not likely to meet with your management team or to be influenced by your growth strategy. They’re beholden to the indices they track.

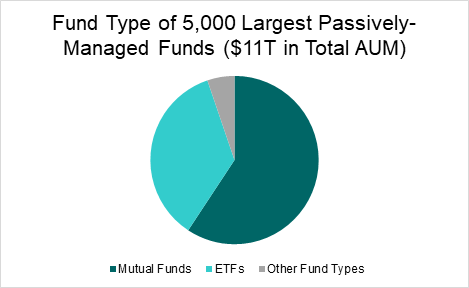

2. What is the makeup of passive funds?

- The 5,000 largest passive investment funds we studied collectively represent total assets under management (AUM) of roughly $11 trillion. The majority (60%) of that AUM is owned by open-ended mutual funds with another 36% in ETFs. The remaining 4% of AUM is in specialty and value funds, which, unlike most passively managed funds, tend to be non-indexed.

3. Is passive ownership more common among companies of a certain size?

- Yes. And SMID-cap (small and mid-cap) companies—including members of the S&P 400 and Russell 2000—fall right into the Goldilocks range.

- We looked at companies of varying market capitalization across four major stock indices: the S&P 500, S&P 400, Russell 2000, and Russell MicroCap. We found that microcap companies are usually too small to be included on major indices, so they tend to get left out the common mutual funds and ETFs. While large- and mega-cap companies are included in the indices, their passive ownership is often offset by significant retail holdings. Apple, for instance, is only 58% owned by institutions, insiders, and corporations (via FactSet, as of 3/31/2021). The remaining portion is largely made up of retail investors.

- In the middle are the SMID-cap companies. These organizations benefit from index inclusion, but generally have less retail ownership, providing the perfect recipe for a disproportionately high degree of passive ownership.

4.Does passive ownership = greater volatility?

- No. And, if anything, the reverse is true. Our research shows that companies that have higher share price volatility have a mild negative correlation with passive ownership.

- This isn’t all that surprising. Passive investors gravitate more toward non-volatile stocks compared to active managers, who typically aim to buy low and sell high. Passive investors tend to have longer investment horizons, so steady and slightly positive alpha is far more advantageous for them. This suggests that passively owned stocks are not necessarily non-volatile because of passive ownership. Rather, passive investors are attracted to stocks that are already non-volatile because such stocks support their investment objectives.

5. Does high passive ownership increase the risk of an activist campaign?

- Not really. Our research shows very little correlation between a company’s passive ownership and its historical number of activist campaigns. What correlation we did find was negative (-0.11).

- However, this in no way suggests that passively owned companies are completely insulated from investor activism. Furthermore, when an activist does get involved in a company with high passive ownership, it’s not likely to be pretty. This Harvard Law study shows that increased passive ownership is positively correlated with certain types of activism. Namely, it’s associated with a higher likelihood of activist campaigns designed to change corporate control or influence (such as board representation) rather than to drive changes in corporate policies. Activism in passively owned companies is also more likely to involve hostile and expensive tactics as opposed to your run-of-the-mill shareholder proposals. Finally, the study shows greater activist success in achieving a settlement with corporate leadership. So, while activism might not be more likely just because you have a high degree of passive ownership, when it does occur, you could be in for a real fight.

- The Engine No. 1 story provides another indicator of how the role of passive investors in activism could be changing. In June, the newly-formed asset manager won three seats on Exxon Mobile’s board after a contentious proxy battle, and it has recently announced that it is launching an ETF (Engine No. 1 Transform 500 ETF) to encourage “transformational change at public companies.” This fund’s explicit purpose is to use activist tactics to drive positive ESG action in its portfolio companies. Again, although passive investors have not represented significant shareholder activism threats to companies to date, stories like this illustrate how the landscape could quickly evolve in the coming years.

How to tailor your investor relations strategy for passive investors

Both the data and our experience show that passive ownership does not necessarily increase the risk of volatility or activism attacks. However, the numbers also indicate that passive investing will continue to gain popularity and that the focus of passive funds will continue to evolve. Issuers, and especially SMID-cap issuers, can take several steps to ensure their investor relations strategies keep pace.

- First, always keep the pulse of the market. Passive investing dictates the majority of the market, and if your company happens to have particularly high passive ownership, it is critical to know the portion of your stock owned by passive investors as well as to monitor the performance of your stock price against relevant indices. This will help you gauge the impact of passive investors and how underlying market conditions may be causing short term volatility in your stock price. While you can’t control macro-economic conditions, you can certainly be prepared for the fall out. And the more you know, the better you’ll be able to answer challenging questions from senior management.

- Religiously update your disclosures. Transparency helps boost the confidence of all investors—passive and active alike—and it decreases speculation and/or mistrust from Wall Street. By keeping disclosures readily available, accessible, and updated, all potential investors looking to get into the stock will have the information they need to make well-informed investment decisions. Furthermore, by creating tailored disclosures for passive investors focused on non-financial metrics, your IR program can spend less time and effort addressing the concerns of passive fund managers. Instead, you can dedicate your focus toward engaging a more diverse set of active funds.

- Come to proxy season well prepared. Even if passive investors don’t want to hear your side of the story, you need to know theirs. Make a habit of monitoring investment stewardship and proxy-voting documents so you can gain a better understanding of passive investors’ historical voting patterns. Specifically, be sure to:

- Use ISS or Glass-Lewis to understand the industry standards for best-in-class corporate policies. Doing so, and ensuring your practices align with the recommendations of proxy advisory firms, will help to ensure passive investors vote in your favor.

- Make sure a senior leadership taskforce thoroughly reviews any existing activist proposals. The goal should be to fairly judge if the proposals act in the best interest of your company. Where possible, settling behind closed doors is generally preferable.

- Monitor voting policy documents of the largest passive owners in your stock. This can help you stay ahead of any changes to firmwide policies that could affect an upcoming vote.

- Pay particular attention to corporate governance. Research shows that passive investors tend to vote more on topics related to corporate governance. You won’t have luck engaging directly with passive fund managers, but you can often drive dialogues with the corporate governance teams at large asset management where your passive owners may reside. This is well worth the effort because it allows your management team to proactively broach issues or concerns pertaining to corporate governance, and it also demonstrates a willingness to make the appropriate changes to satisfy passive investors. This can go a long way toward reducing activism risks come proxy season.

- Finally, don’t forget about the investors who are actively listening to your story. You may not be able to control the amount of passive ownership in your stock—or directly influence the decisions of these investors—but you can most certainly control the Street’s perception of your company’s growth strategy. Put your efforts where they will make the most difference by campaigning harder with active investors. Leverage multipurpose quarterly communications not only to summarize your financials, but also to detail your long-term corporate narrative and strategic investment proposition.

Your investors may be primarily passive, but your IR strategy can’t be

While you don’t have the luxury of sitting down face-to-face with the passive fund managers who may hold the majority of your company’s stock, it’s a mistake to believe there’s nothing you can do to maintain these investors. By doing your homework, making detailed information easily accessible, and finding ways to indirectly influence passive management decisions, you can maximize the benefits of passive investment and avoid being blindsided by some of the pitfalls. If you have questions or would like to know more about our research or perspective on passive investing, give us a call. We’re ready to help you optimize your relationships with all of the various stakeholders in your business.

Want to get additional insights direct to your inbox?

Subscribe to Riveron Insights and get relevant news and trends shaping the world of finance, accounting, and operations