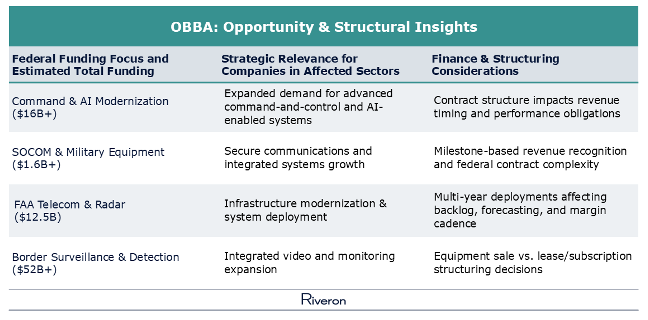

Questions Leadership Teams Should Be Asking

As funding opportunities expand, thoughtful finance leaders may consider:

- How will alternative contract structures (including those involving primes or resellers) affect revenue cadence and margin profile?

- Does our reporting infrastructure provide sufficient visibility into bundled or multi-element arrangements and any required pricing disaggregation?

- Are forecasting processes calibrated for multi-year federal programs or milestone-based billing, and renewal timing variability?

- Have we evaluated how audit scrutiny and disclosure expectations may evolve as program size increases?

- Do commercial, accounting, and FP&A teams have shared clarity before commitments are finalized?

- Is the organization fully capturing any potential tax benefits related to OBBBA funding? (See below for more details on tax considerations).

These are practical guardrails that support informed decision-making. Companies entering or expanding within OBBBA-funded programs, particularly those handling DoD contracts or deploying cloud-based capabilities to federal agencies, should anticipate parallel cybersecurity compliance obligations that scale with contract volume and complexity. CMMC certification requirements and FedRAMP authorization mandates do not relax as award activity accelerates; organizations that underestimate DFARS flow-down requirements or delay compliance investment often face costly remediation costs and program eligibility exposure that offset the revenue opportunity itself.

Alignment Through Execution

Well-informed structural decisions still require disciplined follow-through. As new models are operationalized:

- Accounting treatment must remain consistent with commercial intent

- Budgeting, forecasting and FP&A frameworks must reflect revised revenue cadence

- Documentation and controls must scale alongside program complexity

Maintaining this alignment during execution preserves reporting stability and supports confident communication with investors, regulators, and boards.

The Tax Dimension: OBBBA Provisions Finance Leaders Should Evaluate

OBBBA introduces several tax considerations that intersect directly with contract structure, capital deployment, and M&A planning. Restoration of immediate R&D expensing under Section 174 affects how development programs tied to federal contracts are costed and tracked across entities. Reinstated 100% bonus depreciation under Section 168k accelerates the tax profile of equipment-heavy deployments and requires coordination with cost accounting standards. Made-in-America provisions place new emphasis on supply chain and manufacturing footprint decisions tied to procurement eligibility. The return to an EBITDA-based limitation under Section 163(j) reshapes interest deductibility assumptions in acquisition models and capital structure planning.

Capturing these benefits often depends on how contracts, entities, and cost structures are set up early in the process rather than when programs are deeply underway. Finance leaders should evaluate whether existing policies, data structures, and intercompany frameworks are positioned to capture these benefits as contract strategies evolve.

A Practical Perspective

Federal funding expansions create opportunity. They also introduce complexity that sits squarely within the CFO’s remit. Organizations that evaluate revenue, margin, reporting and tax implications early — and carry that discipline through implementation — position themselves to scale without introducing unnecessary strain.

Finance leadership teams should model structural decisions before they are embedded. This strategic view can then inform execution, so that everything from contract structure to forecasting and reporting assumptions can be aligned before scaling begins. Approaching OBBBA-driven opportunities with financial clarity and aligning accounting and forecasting processes can ensure that leaders implement growth initiatives with confidence.

/Passle/66b0e16610008cf7be5e944d/SearchServiceImages/2026-06-09-14-49-47-330-6a28280be92742e48e7a92ea.jpg)

/Passle/66b0e16610008cf7be5e944d/SearchServiceImages/2026-05-29-18-30-52-023-6a19db5cd80437c18c40c764.jpg)