The article first appeared in ABL Advisor.

As companies, private equity firms and lenders continue through pandemic-driven uncharted waters, much has been written and discussed about the importance of preserving liquidity and navigating the tenets of the CARES Act, and rightly so – these are times to practice fundamentals. At the same time, there is so much more to consider as the old playbook is set aside for new, creative, and collaborative thinking and approaches.

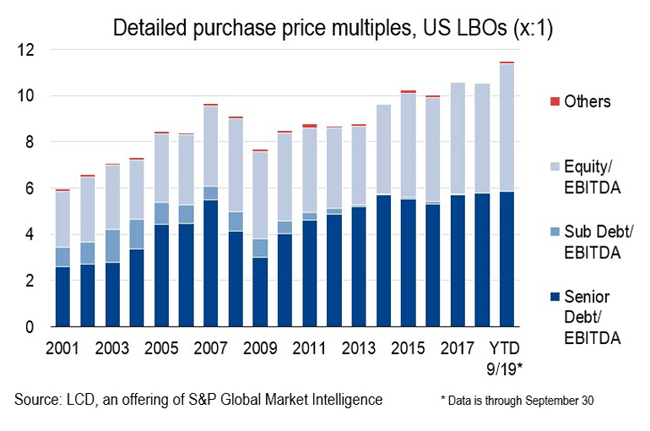

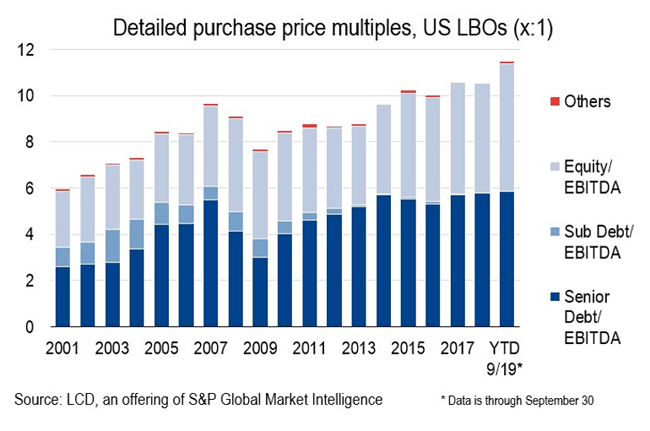

It all comes at a precarious time for many. Just as the non-performing second/third generation middle-market family-owned businesses were the source of many turnarounds and restructurings in the 1990s and 2000s, certain private equity firms overpaying for their recent leveraged acquisitions (refer to chart) in a competitive high EBITDA multiple middle market environment are fueling new sources of potential crisis. Especially susceptible, of course, are the PE firms investing in traditional manufacturing and brick and mortar retail businesses.

At the same time, a considerable number of PE firms are dealing with leadership and ownership transition issues as firm founders/original general partners looks to transition ownership and control to the next generation within the PE firm and/or outside minority stake investors.

The rapid worldwide assent of the COVID-19 Pandemic may have moved up the timetable even more as we proceed through this current global recession of unknown length.

Communication, Collaboration is King

This pivot to collaboration between corporate management, PE and the lender community is essential, and I see it and practice it daily in my oft-rendered role of interim CFO. That is not to say that collaboration has never before been in existence. Yet today it is absolutely essential. After all, we are all in this together.

Last year, I was involved in a liquidation involving a prominent PE firm and multiple lenders. The troubled company manufactured a product that was seasonal and suffering. It was a very difficult negotiation as we sought extra funding in order to buy time. In the end, the company was given no latitude and was taken over. Fast-forward to more recent work with a supplier who lost a key contract and had to downsize. In this instance, and in this era of new, COVID-19 spawned realties, the lenders were more willing to take a look at potential solutions, albeit once they were convinced through communication and transparency that options for maximizing cash flow in the short and long term existed and were viable.

Indeed, we are in a new era, playing on a different field. As such it is behooving all parties to come to the negotiation table open minded, creative and informed; ready to research, uncover and unlock every and any opportunity – from tax refunds to remedies for troubled loans and more. Within a dark cloud there is a potential silver lining IF the situation is approached correctly. The time is now for new ideas and proactivity.

The New Playbook

It starts with the basics. And right now, that means staying on top of the CARES legislation and determining what is available for potential remedies through that legislation, including forgivable loans for keeping people on the payroll. Look at how best to stay liquid. Communicate with customers on invoices and collections.

Being keenly aware that key stakeholders (including lenders) are likely struggling with similar aspects of their own business will often create an easier negotiating platform than usual.

Communication is also key with the lender community – in fact, it is more vital than ever. Providing insight into daily tactics and projections aimed at managing liquidity and controlling discretionary spending. Putting planned projects on hold or anything with a long-term payback. You need to focus on the “right here and the right now” in as open and proactive a way as possible.

“Hey, Lender X, I wanted to give you a heads-up on our latest projections and variances. We will provide you with one projection that assumes 30% new business the rest of the year. We also anticipate you would want to see a more conservative scenario, assuming new customers are not going to move from existing vendors in troubled times. So, we’ll give you a breakeven analysis in a base-case and in a worst-case scenario.”

It’s anticipating what the lender needs to see and hear and getting all of the facts on the table – the good, the bad and the ugly. If there are holes in the liquidity, let’s examine them and figure out how best to handle the situation. What are potential solutions to these problems? Often, it is about how to most effectively share and thus minimize the pain. How can resources be maximized? Restrictions temporarily relaxed? After all, everyone is hurting with one common and unforeseen enemy. There is no blame game going on here. At the same time there is no hiding behind COVID-19 or using it as a scapegoat to shield previous mismanagement or poor business decisions. Rather, it is a time for honesty, conversation and total transparency.

Take, for example, the CARES remedy for ongoing payroll taxes where a portion of the tax can be deferred to help cash flow. Now, eventually you are going to have to fund that deferred liability down the road, this is not a forgivable loan. Moreover, as the tax represents a personal liability to officers, you should put that into a segregated account with the agreement that those funds cannot be touched under any circumstances and educate your lending officer accordingly. Even though the net cash flow might then improve by $30,000 per week because of this payroll tax deferral, these funds should not be utilized for other operating costs.

Nor is this the time to open new bank accounts (not tied to an existing lender agreement) and squirrel away dollars for a secret war chest. Credibility will be lost.

It is also important to be flexible, nimble and ready to adapt and evolve at a moment’s notice. Closely monitor market trends. Keep them in perspective, especially stock market gyrations. The S&P 500 might be indicating the emergence of a bull market; but is it just a sucker’s rally or the beginning of something else?

Thou Shalt Not

While there are absolutely best practices for these times, what should companies and business owners not be doing? We’ve talked about not hiding information or embarking on a strategy that the bank is not made aware of. Here are a few additional areas to consider:

- Mergers & Acquisitions: Thinking of taking action? Don’t act too hastily. Even when under intense financial pressure, you need some type of “face time” to look a potential partner or acquirer/acquiree in the eye. Can you trust someone you have perhaps only met virtually or on a call? Slow down until you can actually sit down across the table from someone and really hash things out, understanding that this may be weeks out.

- Major Projects/Capital Expenditures: Again, slow down and consider all factors carefully when contemplating a big commitment that would cause a cash outflow. This also dovetails with valuation issues as valuing any transaction is very difficult in today’s marketplace. Patience is a virtue. So is being cautious and prudent – and your lenders will appreciate it.

- Risk Management: Don’t rest on laurels here. A big part of risk management is your insurance so check your insurance policies. You could have business interruption benefits coming. Are certain policy premiums based on business activity that might be reduced? Have you recently sold off particular assets that no longer need to be insured? Check the paperwork and the fine print.

- The “Day-to-Day”: It is easy – perhaps even human nature – to fall back into a rigid routine as a way of coping with stress and crisis. Don’t do it. Now is the time for leadership, including CEOs, CFOs and controllers, to devote more time (perhaps 25-50 percent) to seeking creative ways to stay informed and, in turn, work to live another day. Stay informed – including the shifting developments on what our Federal, State and local governments are saying, doing and mandating.

At the same, time, be even more attentive to the nuts and bolts of the day to day. Make sure your numbers are accurate and the books are solid. And if that means taking extra time to make sure all receivables are collected and there are no surprises, then take it. Used to relying on emails? Pick up the phone. Used to bi-weekly meetings? Make them weekly or even daily if necessary. Move beyond your comfort zone – even consider talking to your competition – to seek out additional perspectives and bounce ideas around.

Final Thoughts

There is an old adage that says: “People want to do business with people they know and trust.” Today, it could not be more apropos. If you have not in a while, dust off the old tenets and “tried and trues” of commerce and operational strategy and let them form a strong foundation on which to build new approaches and creative thinking.

We will get through this. But before we can come out of more possible government-imposed isolation, we must embrace change and an openness to pivoting and evolution. That is the real key to survival.

Ready to connect?

As companies, private equity firms, and lenders continue through pandemic-driven uncharted waters, much has been written and discussed about the importance of preserving liquidity and navigating the tenets of the CARES Act.

Connect with an Expert